A Tax-Exempt Life

Corporate Investment Reallocation Using Life Insurance

The Problem: Taxable Corporate Investments and Concentration Risk

You own a private corporation with significant assets invested in taxable, fixed-income investments. Over time, this has created:

- High ongoing tax on passive investment income

- Overexposure to a single asset class

- Reduced access to the Small Business Deduction (SBD)

- Concern about preserving and maximizing estate value for your beneficiaries

You want to diversify your corporation’s assets, maintain liquidity, and reduce tax — without sacrificing long-term stability or control.

The Solution: Corporate Investment Reallocation

The Corporate Investment Reallocation strategy uses corporate-owned permanent life insurance to reposition a portion of your fixed-income investments into a more tax-efficient structure.

This approach helps:

- Diversify your corporate balance sheet

- Reduce tax on passive investment income

- Preserve liquidity and access to capital

- Increase the after-tax value of your estate

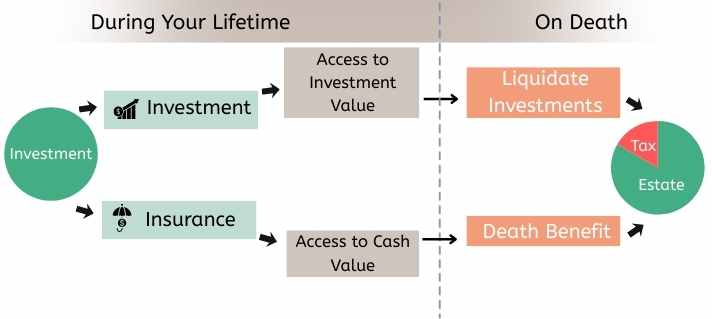

How Corporate Investment Reallocation Works

- Your corporation purchases a permanent life insurance policy on your life.

- The corporation owns the policy.

- The corporation pays the premiums.

- The corporation is the beneficiary.

Corporate funds currently held in taxable fixed-income investments are reallocated to fund the policy over time.

The policy provides both life insurance protection and tax-advantaged cash value growth inside the corporation.

Key Benefits of Corporate Investment Reallocation

1. Tax-Preferred Cash Value Growth

Cash values inside a permanent life insurance policy grow on a tax-deferred basis. By shifting a portion of fixed-income investments into insurance:

- Annual tax on investment income is reduced

- Exposure to the Tax on Passive Income Rules may be lowered

- The corporation may preserve access to the Small Business Deduction (SBD)

- Overall portfolio volatility can be reduced through diversification

2. Liquidity and Access to Capital

Despite being an insurance strategy, liquidity is preserved. If the corporation needs access to capital, options may include:

- Policy loans

- Withdrawals from the policy

- Assigning the policy as collateral for a third-party loan

In many cases, up to 90% of the policy’s cash value may be accessible. Cash values may also offer higher collateral value than traditional investment portfolios.

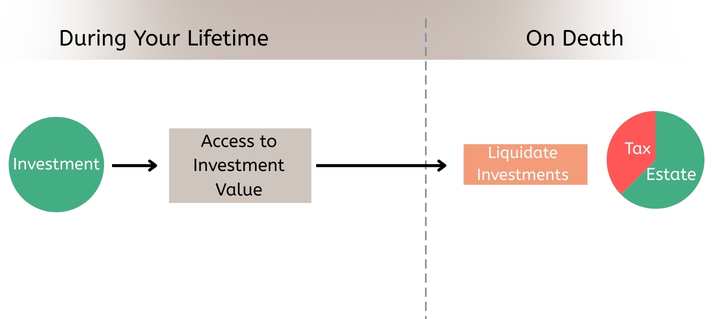

3. Tax-Efficient Estate Transfer

On death:

- The tax-free death benefit is paid to the corporation

- The death benefit (minus the policy’s Adjusted Cost Basis, or ACB) is credited to the corporation’s Capital Dividend Account (CDA)

- An amount equal to the CDA can be paid to shareholders tax-free as a capital dividend

- Any remaining funds can be distributed as taxable dividends

Even if part of the death benefit is used to repay a loan, the full death benefit is generally credited to the CDA, subject to ACB rules.

When to Consider Corporate Investment Reallocation

This strategy may be appropriate if you:

- Are a shareholder or key person of a Canadian-Controlled Private Corporation (CCPC)

- Hold significant assets in a corporate fixed-income or GIC portfolio

- Want to diversify your corporate investments

- Are seeking to reduce tax on corporate passive income

- Need corporate life insurance but don’t want to give up liquidity

- Want to maximize the after-tax value of your estate

Important Considerations

Corporate Investment Reallocation involves insurance, tax, and legal planning. Policy loans, withdrawals, and collateral strategies may have tax implications.

Always consult with your tax, legal, and insurance advisors before implementing this strategy to ensure it aligns with your corporation’s objectives and circumstances.